The manufacturing account format is a crucial tool for tracking production costs and determining a company’s manufacturing performance. In this article, we delve into the details of this essential financial statement. It provides a clear breakdown of direct and indirect costs involved in the production process. Understanding the manufacturing account format is key to making informed decisions and optimizing efficiency in manufacturing operations. Let’s explore how this format can empower businesses to manage their manufacturing processes effectively.

Exploring the Manufacturing Account Format: A Comprehensive Guide for Beginners

Welcome, young learners! Today, we are going to dive into the fascinating world of manufacturing account format. Have you ever wondered how companies keep track of their production costs and profits? Well, the manufacturing account format is the key to understanding this process. So, let’s roll up our sleeves and explore the ins and outs of manufacturing accounts together!

What is a Manufacturing Account?

Before we delve into the format of a manufacturing account, let’s first understand what it actually is. A manufacturing account is a financial statement that helps businesses in the manufacturing industry track their production costs and calculate their profits. It provides a detailed breakdown of all the costs incurred during the manufacturing process, allowing companies to analyze their performance and make informed decisions.

The Importance of the Manufacturing Account

Now, you might be wondering why a manufacturing account is so important. Well, think of it as a detailed recipe that helps a chef keep track of all the ingredients used in a dish. Similarly, a manufacturing account allows businesses to monitor their expenses, identify areas where costs can be reduced, and ultimately improve their profitability. By maintaining accurate manufacturing accounts, companies can make strategic decisions that drive their success.

Components of a Manufacturing Account

So, what exactly goes into a manufacturing account? Let’s break it down into the key components:

1. Direct Materials

The first component of a manufacturing account is direct materials. These are the raw materials that are directly used in the production process. For example, if a company manufactures wooden furniture, the wood used to make the furniture would be considered a direct material. Keeping track of these materials is crucial for calculating the total cost of production.

2. Direct Labor

Next, we have direct labor. This includes the wages of workers who are directly involved in the manufacturing process. For instance, the carpenters who assemble the wooden furniture would be considered direct labor. By including direct labor costs in the manufacturing account, companies can accurately determine the labor component of their production expenses.

3. Manufacturing Overheads

Manufacturing overheads refer to all the indirect costs associated with the manufacturing process. This can include expenses such as factory rent, utilities, depreciation of machinery, and maintenance costs. By allocating manufacturing overheads to the production process, companies can get a comprehensive view of the total expenses incurred in manufacturing goods.

The Format of a Manufacturing Account

Now that we’ve covered the components of a manufacturing account, let’s explore the format in which this information is typically presented. A manufacturing account is usually structured in the following manner:

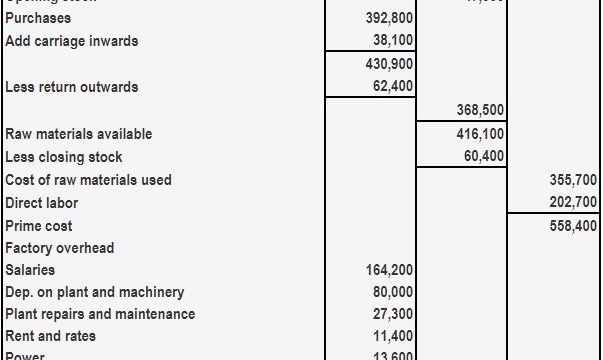

Opening Stock of Work-in-Progress

This section accounts for any unfinished goods from the previous accounting period that have been carried forward into the current period. It reflects the value of work that has already been started but not completed.

Direct Materials

Here, the cost of direct materials used in the manufacturing process is recorded. This includes the purchase cost of raw materials that have been transformed into finished goods.

Direct Labor

The direct labor costs associated with manufacturing activities are listed in this section. This includes the wages of employees directly involved in producing goods.

Manufacturing Overheads

All indirect manufacturing costs, such as factory rent and utilities, are accounted for in this part of the manufacturing account. These overhead costs are essential for calculating the total cost of production.

Prime Cost

The sum of direct materials, direct labor, and manufacturing overheads gives us the prime cost, which represents the total cost of production before taking into account any selling and administrative expenses.

Work-in-Progress (Ending Stock)

This section deals with any unfinished goods at the end of the accounting period. It reflects the value of work that is in progress but not yet completed.

Cost of Goods Manufactured

By subtracting the opening stock of work-in-progress and adding the ending stock of work-in-progress from the prime cost, we arrive at the cost of goods manufactured. This figure represents the total cost of finished goods produced during the period.

Finished Goods Stock Account

Finally, the cost of goods manufactured is transferred to the finished goods stock account, which tracks the value of completed goods that are ready for sale.

In Conclusion

Congratulations, young learners! You’ve now gained a solid understanding of the manufacturing account format and its significance in the business world. By mastering the art of creating and analyzing manufacturing accounts, you’re one step closer to unraveling the mysteries of financial management in the manufacturing industry. Keep exploring, keep learning, and who knows, maybe one day you’ll be the mastermind behind a successful manufacturing enterprise!

Happy accounting!

MANUFACTURING ACCOUNTS (PART 1)

Frequently Asked Questions

What is the purpose of a manufacturing account format?

The manufacturing account format is used by companies to summarize the costs involved in the production process. It helps in calculating the cost of goods manufactured.

How is a manufacturing account format different from a trading account?

A manufacturing account format focuses on the production costs of goods, including raw materials, labor, and overheads, while a trading account deals with buying and selling finished goods.

What are the typical sections included in a manufacturing account format?

A typical manufacturing account format includes sections for opening stock, direct materials consumed, direct labor, factory overheads, and closing stock.

How does the manufacturing account format help in cost control?

By detailing the various costs involved in manufacturing, the format allows companies to analyze expenses and identify areas where cost-saving measures can be implemented, thus aiding in cost control.

Final Thoughts

In conclusion, the manufacturing account format is a vital tool for businesses to track production costs accurately. It consists of sections such as direct materials, direct labor, and manufacturing overhead. By organizing expenses in this structured format, companies can analyze their manufacturing processes efficiently. Implementing a clear manufacturing account format enables businesses to make informed decisions and improve cost control strategies effectively.